It’s hard to imagine the coming year. It’s kind of like trying to light a gas stove for five minutes with wet matches and then find a dry one. It could be illuminating.

Republicans and the Democrats are blaming everything that’s wrong in the country on each other. The idea that there can be two ways to get to the same destination seems to elude the politicians and most of the voters. "Right" and "wrong," are concepts that are interpreted differently, depending on the person’s situation. Very few wars are “right,” but there have been a few that I would deem as having been “necessary.” To a Marine in Iraq, “necessary” is also an arguable term.

The new push for health care seems, to be the last straw for the camel’s back. We can’t pay for it now; legislation won’t make it any cheaper. If you ever need to visit the emergency room for treatment and have a credit card, go to Urgent Care (there is no 8 hour wait). The 35 and under crowd would just love a health insurance program; you get taxed for getting old while you’re still young enough to pay for it.

Tomorrow the minimum wage goes up 50 cents and a restaurant with 20 employees has an extra $50k per year in costs. Congress meant well, god bless ‘em, one less employee is not quite what they had in mind.

Real estate is beginning its great decline. Remember that bank foreclosures count as a house sale when you view real estate statistics. This distorts the number of actual buyers. As prices drop, more people will become upside down in their loans. Those that bought into the market in the last five years with ten percent or less down, have real issues (we’re not talking magazine subscriptions).

Unemployment in the coming year could be quite low. Los Angeles is reporting another year of decreasing crime. It more or less suggests a significant drop in adults in the 17-30 age group, not more effective crime prevention. The labor pool is contracting; add to that, the baby boomers reaching retirement. This could force wages up.

Food costs are increasing drastically. A dozen eggs have gone from 99 cents to $1.50 in the last two months with a sign in the window “limit two dozen.” Granted, eggs have been $2.69 a dozen at Ralph’s for years, I just don’t buy my eggs there. The damn chickens got a pay raise and I didn’t!

The big difference between a blog and the news is; we are suggesting what may happen in the future, whereas the Newspapers and TV report what has happened. We are looking forward and they are examining the past. The news media needs, “Who, What, Why, When and Where,” for a story. Without it, it ain’t news. A blog is kind of like little Johnny telling Daddy that Mommy’s been fooling around. Daddy needs a name before he loads the hand gun. When he pulls the trigger you have all 5 W’s. Now that's news!

The good thing about all of this for next year is that this is only a blog. So, "No News is Good News!"

Have a Happy New Year Everyone!

Monday, December 31, 2007

Tuesday, December 25, 2007

The Social Security Medicare Headache

Current financial news suggests the economy is deteriorating. Many institutions are in damage control mode. If an entity is facing an impending bankruptcy, why announce it early? Collect a few more paychecks. People tend to hide problems. Sweep this under the rug and maybe it will go away. The real picture of our predicament is probably still well hidden. Nothing is a clear as it seems. No set of facts describes the whole story. And when you mix and match news reports, there is room for the error of interpretation

People talk about helicopter Ben throwing money out everywhere. It makes a great newspaper story, but it’s way out in left field. All he can do is make the money easier to borrow. The damn problem is you can’t force people to borrow money. If you want to blame Ben for what Congress has spent, be my guest. He is being groomed to take the fall.

Congress is the main player in this game as it unfolds. To get elected they promised the moon and pretty much delivered. This group repealed laws written in the 1930’s that could have kept a lot of this from happening a second time. The country is headed into a deflationary recession but our elected “Cesspool of Irresponsibility” could change all of that. Congress assumed (with good reason) that the tax receipts would increase each year. Even with inflation, they will probably drop next year. Fixed Costs are the real headache. The amount spent on social programs is pretty much set in stone (it isn’t going to get smaller) 56% (See diagram). As tax revenues decrease, the pie gets smaller; the share devoted to social programs increases. A 20 percent decrease in revenues would make the fixed cost rise to 70 percent of the budget.

Congress will have some very unpleasant decisions to face\avoid (choose one) in the near future. Don’t expect them to cut Social Security or Medicare; they want to get re elected. Congress is held accountable for fixing present problems, but responsibility for the future problems doesn’t even enter the equation. From there it is quite simple; the Treasury writes the checks to cover the fixed costs. This is where the money is printed. It’s kind of like a Visa card with no limit on it.

Where will Congress cut when things get worse? There is no answer to that question yet. When FDR was elected, there were no social programs, and by 1948, these programs consumed 10% of the budget. Now where are we? Entitlements are where the cuts will have to be made. To a Congressman, that’s an incredibly stupid suggestion especially come election time.

We are looking at several things in decline; credit, housing, banking and a shrinking tax base. Just think, you got all this, in time for Christmas!

Merry Christmas everyone.

People talk about helicopter Ben throwing money out everywhere. It makes a great newspaper story, but it’s way out in left field. All he can do is make the money easier to borrow. The damn problem is you can’t force people to borrow money. If you want to blame Ben for what Congress has spent, be my guest. He is being groomed to take the fall.

Congress is the main player in this game as it unfolds. To get elected they promised the moon and pretty much delivered. This group repealed laws written in the 1930’s that could have kept a lot of this from happening a second time. The country is headed into a deflationary recession but our elected “Cesspool of Irresponsibility” could change all of that. Congress assumed (with good reason) that the tax receipts would increase each year. Even with inflation, they will probably drop next year. Fixed Costs are the real headache. The amount spent on social programs is pretty much set in stone (it isn’t going to get smaller) 56% (See diagram). As tax revenues decrease, the pie gets smaller; the share devoted to social programs increases. A 20 percent decrease in revenues would make the fixed cost rise to 70 percent of the budget.

Congress will have some very unpleasant decisions to face\avoid (choose one) in the near future. Don’t expect them to cut Social Security or Medicare; they want to get re elected. Congress is held accountable for fixing present problems, but responsibility for the future problems doesn’t even enter the equation. From there it is quite simple; the Treasury writes the checks to cover the fixed costs. This is where the money is printed. It’s kind of like a Visa card with no limit on it.

Where will Congress cut when things get worse? There is no answer to that question yet. When FDR was elected, there were no social programs, and by 1948, these programs consumed 10% of the budget. Now where are we? Entitlements are where the cuts will have to be made. To a Congressman, that’s an incredibly stupid suggestion especially come election time.

We are looking at several things in decline; credit, housing, banking and a shrinking tax base. Just think, you got all this, in time for Christmas!

Merry Christmas everyone.

Sunday, December 23, 2007

A Bank that couldn't say No

Let’s take Citigroup and look at their balance sheet. Two trillion in assets, these are customer deposits. The bank has about 127 billion worth of equity (book value $25.479 times the number of shares 4.98 Billion). Don’t confuse this with “market cap” which is the number of shares times the current stock price (152.92 Billion). Market cap could go to a dollar and it would not affect the book value of the company. As a stockholder you could end up with zip. If you hold preferred stock, you are ahead of widows and orphans. Abu Dhabi has preferred stock.

In order to pay a reasonable interest rate, the money has to be invested in some vehicle that has a decent return. It’s a good assumption the bank didn’t invest the 1.9 trillion in Treasury bills or other government bonds; the return is just not there. In three months time, Citigroup has come up with a write-down of bad investments with a total somewhere between 72 billion to 100 billion dollars (see Deutsche Bank spread sheet).These are real estate SIV’s and CDO’s. What happens if we move out another four months? Citigroup’s fiscal year ends in December. How liquid are their assets? The answer to that question is a little like taking a laxative to cure diarrhea. If you think it’s bad now, wait a while.

---Courtesy Deutsche Bank November 11, 2007. Double click for larger image

---Courtesy Deutsche Bank November 11, 2007. Double click for larger image

What did Citigroup invest the rest in? If it wasn’t “invested” in real estate, then where did they put it? Credit card loans or how about hedge funds, both are "real money makers." What ever it is, it is probably not easily convertible to cash.

Can a bank have 100 billion in losses and still be functional? There hasn’t been a peep from Federal regulators. It seems a little like the Donald Trump wing ding of several years back. If the banks had foreclosed on him they would have gotten very little. Instead they loaned him more money and rewrote his loans.

Are the Federal Bank examiners checking the books? They had a rough time with the 125 billion dollar Savings and Loan bailout of the 1990’s. Citigroup is BIG and we are only talking one bank. A bank in trouble is like spotting one cockroach, you know there has to be more.

The amount of money involved in losses is staggering. The amount of money this one bank controls is beyond comprehension. Am I the only one that thinks this needs to be examined more closely? Have I mistakenly reported billions when they actually meant millions? No, the figures are real and big.

Just examine the Federal Reserve handing out banking reserves, without naming names (to keep banks from being embarrassed???) at emergency auctions? We could be looking at money leaving the banks at a rate faster than they can liquidate assets. "Emergency auctions" sounds like “Man the Lifeboats.”

The banking crisis is a little like the Hindenburg. It could go from something to nothing real fast. The only trouble is, who owns the something that's about to become nothing.

In order to pay a reasonable interest rate, the money has to be invested in some vehicle that has a decent return. It’s a good assumption the bank didn’t invest the 1.9 trillion in Treasury bills or other government bonds; the return is just not there. In three months time, Citigroup has come up with a write-down of bad investments with a total somewhere between 72 billion to 100 billion dollars (see Deutsche Bank spread sheet).These are real estate SIV’s and CDO’s. What happens if we move out another four months? Citigroup’s fiscal year ends in December. How liquid are their assets? The answer to that question is a little like taking a laxative to cure diarrhea. If you think it’s bad now, wait a while.

---Courtesy Deutsche Bank November 11, 2007. Double click for larger image

---Courtesy Deutsche Bank November 11, 2007. Double click for larger imageWhat did Citigroup invest the rest in? If it wasn’t “invested” in real estate, then where did they put it? Credit card loans or how about hedge funds, both are "real money makers." What ever it is, it is probably not easily convertible to cash.

Can a bank have 100 billion in losses and still be functional? There hasn’t been a peep from Federal regulators. It seems a little like the Donald Trump wing ding of several years back. If the banks had foreclosed on him they would have gotten very little. Instead they loaned him more money and rewrote his loans.

Are the Federal Bank examiners checking the books? They had a rough time with the 125 billion dollar Savings and Loan bailout of the 1990’s. Citigroup is BIG and we are only talking one bank. A bank in trouble is like spotting one cockroach, you know there has to be more.

The amount of money involved in losses is staggering. The amount of money this one bank controls is beyond comprehension. Am I the only one that thinks this needs to be examined more closely? Have I mistakenly reported billions when they actually meant millions? No, the figures are real and big.

Just examine the Federal Reserve handing out banking reserves, without naming names (to keep banks from being embarrassed???) at emergency auctions? We could be looking at money leaving the banks at a rate faster than they can liquidate assets. "Emergency auctions" sounds like “Man the Lifeboats.”

The banking crisis is a little like the Hindenburg. It could go from something to nothing real fast. The only trouble is, who owns the something that's about to become nothing.

Saturday, December 15, 2007

Next Stop Inflation or Deflation?

Where is the country headed? We seem to be on the Sword of Damocles. Is it inflation or deflation? Where to from here?

In an inflationary scenario, debtors would benefit, it would be easier to pay back money borrowed. Those with savings would feel the tax of inflation. Each dollar would buy less than it use to (what’s new about that). Those on a fixed retirement income would suffer the most. Inflation is a way government can tax everyone. The neat thing is that there is no need for a tax collector. Plus you can’t cheat on your taxes. So when the government prints money, it’s kind of like taking a half bottle of whisky and topping it off with water to make a full quart. The buyer ends up with half the buzz at twice the price. Basically government is taxing one dollar and spending two.

Deflation on the other hand is a rough buggy ride for everyone. It tends to feed on itself and get worse (with government help). The economy slows down unemployment increases, bankruptcies and foreclosures increase. Prices drop and money buys more than it use to. Debts become harder to pay off when jobs are scarce. During the great depression, government services suffered greatly. Teachers, firemen, police and other services were cut severely. Congress could have a very serious problem if revenues from taxes collected decrease dramatically.

On the front page of today’s paper, San Diego readers saw a headline “Governor Schwartznegger set to declare fiscal emergency.” The State has a 14 billion dollar budget shortfall. That and all of the foreclosures suggest deflation is the current direction of travel.

There is just one fine wrinkle. Notice how government tax receipts are decreasing? There are a lot of fixed costs to be paid out, Social Security, Medicare and Medicaid. Uncle Sam has been spending the Social Security taxes as well as the regular taxes and even the gas tax on the yearly budget. When FDR wanted to stimulate the economy in the 1930’s with government spending, none of these liabilities were hanging around the government’s neck. The economy went to full power when Japan “remodeled” Pearl Harbor. Today's fixed costs for government entitlements, may force the government to print the funds necessary. That sort of inflation can spiral out of control.

Congress seems to think that spending is good, worry about the bill later. As government receipts decrease notice how the fixed costs consume a larger part of the pie. It’s a little like the foreclosure mess. Congress can barely pay the bills now, what happens when deflation takes hold? The expression “Between a Rock and a Hard place," comes to mind. Will they turn the dollar into Monopoly Money? Abu Dhabi just bought Baltic Avenue (Citigroup). Bye Bye worthless Dollar, Buy Buy our assets (a pun or two).

In an inflationary scenario, debtors would benefit, it would be easier to pay back money borrowed. Those with savings would feel the tax of inflation. Each dollar would buy less than it use to (what’s new about that). Those on a fixed retirement income would suffer the most. Inflation is a way government can tax everyone. The neat thing is that there is no need for a tax collector. Plus you can’t cheat on your taxes. So when the government prints money, it’s kind of like taking a half bottle of whisky and topping it off with water to make a full quart. The buyer ends up with half the buzz at twice the price. Basically government is taxing one dollar and spending two.

Deflation on the other hand is a rough buggy ride for everyone. It tends to feed on itself and get worse (with government help). The economy slows down unemployment increases, bankruptcies and foreclosures increase. Prices drop and money buys more than it use to. Debts become harder to pay off when jobs are scarce. During the great depression, government services suffered greatly. Teachers, firemen, police and other services were cut severely. Congress could have a very serious problem if revenues from taxes collected decrease dramatically.

On the front page of today’s paper, San Diego readers saw a headline “Governor Schwartznegger set to declare fiscal emergency.” The State has a 14 billion dollar budget shortfall. That and all of the foreclosures suggest deflation is the current direction of travel.

There is just one fine wrinkle. Notice how government tax receipts are decreasing? There are a lot of fixed costs to be paid out, Social Security, Medicare and Medicaid. Uncle Sam has been spending the Social Security taxes as well as the regular taxes and even the gas tax on the yearly budget. When FDR wanted to stimulate the economy in the 1930’s with government spending, none of these liabilities were hanging around the government’s neck. The economy went to full power when Japan “remodeled” Pearl Harbor. Today's fixed costs for government entitlements, may force the government to print the funds necessary. That sort of inflation can spiral out of control.

Congress seems to think that spending is good, worry about the bill later. As government receipts decrease notice how the fixed costs consume a larger part of the pie. It’s a little like the foreclosure mess. Congress can barely pay the bills now, what happens when deflation takes hold? The expression “Between a Rock and a Hard place," comes to mind. Will they turn the dollar into Monopoly Money? Abu Dhabi just bought Baltic Avenue (Citigroup). Bye Bye worthless Dollar, Buy Buy our assets (a pun or two).

Sunday, December 09, 2007

Cash Only

When there is a run on a bank or other financial institution, the target has to raise cash to satisfy redemptions. Usually this entity would be fully invested to max out profit for depositors. To raise cash, the institution would sell its most liquid assets, stocks, bonds, money market funds etc, leaving the dogs, on the hope they improve given time. Notice good assets are redeemed for cash; the crap stays in the vault.

The State Investment Pool in Florida started out two weeks ago with 27 billion and shut the doors December 4th. Eight billion left the fund with no penalty. After the doors opened December 7, another two billion hit the exit turnstile. From Bloomberg

link

This is what killed the banks in the 1930’s. The banking system collapsed not because of bad bank investments (no denying that there were plenty), they collapsed when depositors lost faith in the bank. Those first in line got their money, those last in line, got an education. The FDIC insurance stops the prospect of a bank run and keeps the depositors’ savings intact. These Fund Pools are not banks and are not insured by the FDIC.

An electric utility company and a county government agree to a 2% redemption fee of 1.4 million dollars. Maybe to act responsibly means you have to do things that are painful from time to time. If the investment pool can change the rules after the fact, whose money is it really? Could it be, these two entities examined their future accounts receivable, and figured out that the local economy has a few issues? They seem to know what they are doing. One turns off the lights; the other auctions off foreclosures.

The State Investment Pool in Florida started out two weeks ago with 27 billion and shut the doors December 4th. Eight billion left the fund with no penalty. After the doors opened December 7, another two billion hit the exit turnstile. From Bloomberg

link

Florida schools and towns pulled more than $1.7 billion from a state investment pool in the two days since a freeze on their accounts was lifted, as local governments remained wary of keeping money in a fund with subprime mortgage-tainted holdings . . . . . . . . . . .

BlackRock, hired Nov. 30 to salvage the fund, walled off $2 billion of the weakest investments and imposed restrictions to limit withdrawals, including imposing a 2 percent fee on redemptions that exceed certain levels. Some governments have been willing to pay that price to get their money out . . . . . . . . . . .

Perry, the Jacksonville Electric Authority and Desoto County together paid $1.4 million in penalties yesterday to remove $66.7 million from their accounts . . . . . . . . .

This is what killed the banks in the 1930’s. The banking system collapsed not because of bad bank investments (no denying that there were plenty), they collapsed when depositors lost faith in the bank. Those first in line got their money, those last in line, got an education. The FDIC insurance stops the prospect of a bank run and keeps the depositors’ savings intact. These Fund Pools are not banks and are not insured by the FDIC.

An electric utility company and a county government agree to a 2% redemption fee of 1.4 million dollars. Maybe to act responsibly means you have to do things that are painful from time to time. If the investment pool can change the rules after the fact, whose money is it really? Could it be, these two entities examined their future accounts receivable, and figured out that the local economy has a few issues? They seem to know what they are doing. One turns off the lights; the other auctions off foreclosures.

Thursday, December 06, 2007

The Home Stretch

Lately pundits have been arguing over whether or not we are in a recession. At the same time the housing foreclosure mess is being addressed in the same fashion, as it was during the Great Depression (25 states passed moratorium laws on home foreclosures in the early 1930’s). The phrase “Déjà vu” comes to mind.

This five year moratorium on resets may backfire in a strange but consistent way. In California a few years back, the legislature realized that the spot price for natural gas for the utilities was a lot cheaper than their ten year contracted price. So they decided not to renew the contract and buy on the spot market. When the contracts expired the spot market took off like a rocket. The legislature meant well, it just didn’t turn out like they though it would.

A few years back, Congress passed a law to help farmers write down large farm equipment purchases over five years. Sounded great, every Realtor from here to nowhere bought a Hummer and wrote it off as a business expense.

In essence, teaser/exotic loans are gone, no more 2/28 or 3/27 loans. Everything from here out, is straight missionary style. The banks will draw a red line around California. Financing a home will become more difficult.

The headlines for tomorrow revolve around the five year freeze for home loans. The real story has been overlooked; the banks are in one hell of a mess. The possibility of one million families losing their homes would be tragic but most would be back to the regular old grind within a year. That’s not true for America’s financial banking system. Leave out the FDIC insured stuff. What is left of the rest is probably a USA (Up in Smoke Asset). IRA's and retirement funds come to mind.

I kind of get the feeling that President Bush just held the ribbon cutting ceremony for the Next Great Depression. Notice that you don't need an ambulance for this sort of catastrophe. You go to sleep well off and wake up poor. It's kind of like paying real cash for the hooker you had in your dream last night. It makes absolutely no cents.

This five year moratorium on resets may backfire in a strange but consistent way. In California a few years back, the legislature realized that the spot price for natural gas for the utilities was a lot cheaper than their ten year contracted price. So they decided not to renew the contract and buy on the spot market. When the contracts expired the spot market took off like a rocket. The legislature meant well, it just didn’t turn out like they though it would.

A few years back, Congress passed a law to help farmers write down large farm equipment purchases over five years. Sounded great, every Realtor from here to nowhere bought a Hummer and wrote it off as a business expense.

In essence, teaser/exotic loans are gone, no more 2/28 or 3/27 loans. Everything from here out, is straight missionary style. The banks will draw a red line around California. Financing a home will become more difficult.

The headlines for tomorrow revolve around the five year freeze for home loans. The real story has been overlooked; the banks are in one hell of a mess. The possibility of one million families losing their homes would be tragic but most would be back to the regular old grind within a year. That’s not true for America’s financial banking system. Leave out the FDIC insured stuff. What is left of the rest is probably a USA (Up in Smoke Asset). IRA's and retirement funds come to mind.

I kind of get the feeling that President Bush just held the ribbon cutting ceremony for the Next Great Depression. Notice that you don't need an ambulance for this sort of catastrophe. You go to sleep well off and wake up poor. It's kind of like paying real cash for the hooker you had in your dream last night. It makes absolutely no cents.

Monday, December 03, 2007

Homeowner be Damned

So Henry Paulson is going to freeze the interest rates on home loans and Ben Bernanke is going to lower the Fed discount rate a whole point. It’s kind of like fishing with a shotgun in a glass bottom boat. You get a swimming lesson after you pull the trigger.

What happens when you freeze the interest rates? Go out and try to buy any house with financing, its just isn’t going to be there. What businessman will loan money under fixed assumptions only to be paid under a changing set of rules. Georgia a while back passed a law to protect homeowners and effectively shut down the loan industry in the state. This is the old “Pull the rug out from under the lender routine.”

Then we have Bernanke lowering the Fed funds rate. It doesn't take much thinking to figure out that the exchange rate on the dollar will fall. In this case, smart money will refuse to renew their Treasury Bills. Since it’s competitive bidding, less bidders, means higher prices. There is a couple of trillion dollars that could vote with feet. Foreigners will sell the dollar now and wait. Then buy when it hits bottom. If things don’t go right, this could be like catching a bag of cement dropped from a second floor window (messy to say the least). Treasury bill rates could surge up as soon as tomorrow.

The neat thing about lowering the Fed funds rate, is that any money it does create (ie loans to market makers), won’t be heading for real estate or SIVs, it will be going into the stock market. Google could hit $1000 by Christmas (just a joke, I don’t give investment advice).

So what do we have? A shut down of future real estate financing or the prospect of absurd interest rate financing for home ownership. Flight of foreign capital will raise Treasury rates.

What is really happening at the Bernanke and Paulson level? The banking system could collapse. Unless they can keep the homeowner making payments the game is over. In order to keep the banks from dropping dead, the really bad stuff cannot be allowed to be marked to market.

Step back and think about what has happened in the last two years with Real Estate Bubble Bloggs. Many of them have stopped posting. What they were warning about has happened. It was very obvious even back then. Now, all of a sudden, the Government is concerned about the homeowner? I think not. The banks have a pretty good idea of what’s going to happen three months from now. Citygroup has no equity if you subtract its mistakes from its book value. What’s that mean? The government could be called on to take over an organization that is just about half as big as itself.

Ben and Henry are in that Christmas giving mood, so don’t bend over if you need to refi, just walk away, give yourself and your family some real peace of mind.

What happens when you freeze the interest rates? Go out and try to buy any house with financing, its just isn’t going to be there. What businessman will loan money under fixed assumptions only to be paid under a changing set of rules. Georgia a while back passed a law to protect homeowners and effectively shut down the loan industry in the state. This is the old “Pull the rug out from under the lender routine.”

Then we have Bernanke lowering the Fed funds rate. It doesn't take much thinking to figure out that the exchange rate on the dollar will fall. In this case, smart money will refuse to renew their Treasury Bills. Since it’s competitive bidding, less bidders, means higher prices. There is a couple of trillion dollars that could vote with feet. Foreigners will sell the dollar now and wait. Then buy when it hits bottom. If things don’t go right, this could be like catching a bag of cement dropped from a second floor window (messy to say the least). Treasury bill rates could surge up as soon as tomorrow.

The neat thing about lowering the Fed funds rate, is that any money it does create (ie loans to market makers), won’t be heading for real estate or SIVs, it will be going into the stock market. Google could hit $1000 by Christmas (just a joke, I don’t give investment advice).

So what do we have? A shut down of future real estate financing or the prospect of absurd interest rate financing for home ownership. Flight of foreign capital will raise Treasury rates.

What is really happening at the Bernanke and Paulson level? The banking system could collapse. Unless they can keep the homeowner making payments the game is over. In order to keep the banks from dropping dead, the really bad stuff cannot be allowed to be marked to market.

Step back and think about what has happened in the last two years with Real Estate Bubble Bloggs. Many of them have stopped posting. What they were warning about has happened. It was very obvious even back then. Now, all of a sudden, the Government is concerned about the homeowner? I think not. The banks have a pretty good idea of what’s going to happen three months from now. Citygroup has no equity if you subtract its mistakes from its book value. What’s that mean? The government could be called on to take over an organization that is just about half as big as itself.

Ben and Henry are in that Christmas giving mood, so don’t bend over if you need to refi, just walk away, give yourself and your family some real peace of mind.

Saturday, December 01, 2007

Citigroup is Toast

Several banks are forming a consortium to make a market for SIVs. Citigroup holds about 100 billion dollars worth. Coincidently this is about the amount this group is going to raise. These instruments are a little like intestinal gas. It reminds me of the two immigrants, new to the US, taking notice of several balloons tied to an outhouse door. The one remarks to the other, “I’ve heard them, and smelled them, but this is the first time I have seen one!”

To keep the discussion polite, Citi/Shiti has some balloons for sale. They are rated as Chiti. I know we haven’t lost the short bus group, they all know the “Pull my finger drill.”

Needless to say, where does the 100 billion come from to make the SIVs fungible? The answer is so obvious that it boggles the mind, BAT GUANO FUTURES (Just Kidding). But the people out there that everyone is listening to, expecting a solution from, are part of a certified circus act.

Let’s see, you are a bank and you lost 100 billion dollars. The total cost to tax payers for the S & L fiasco of the 1990’s was only 125 billion. We have one bank with a very bad cough and more obligations on debt than the previous banking brouhaha in total.

What’s a 100 billion? The answer depends on who you ask. The one question not asked, is what bank can survive a 100 billion dollar loss? In my opinion, none. Citigroup is toast.

To keep the discussion polite, Citi/Shiti has some balloons for sale. They are rated as Chiti. I know we haven’t lost the short bus group, they all know the “Pull my finger drill.”

Needless to say, where does the 100 billion come from to make the SIVs fungible? The answer is so obvious that it boggles the mind, BAT GUANO FUTURES (Just Kidding). But the people out there that everyone is listening to, expecting a solution from, are part of a certified circus act.

Let’s see, you are a bank and you lost 100 billion dollars. The total cost to tax payers for the S & L fiasco of the 1990’s was only 125 billion. We have one bank with a very bad cough and more obligations on debt than the previous banking brouhaha in total.

What’s a 100 billion? The answer depends on who you ask. The one question not asked, is what bank can survive a 100 billion dollar loss? In my opinion, none. Citigroup is toast.

Thursday, November 29, 2007

Depression 2006 no Travel Agent Needed

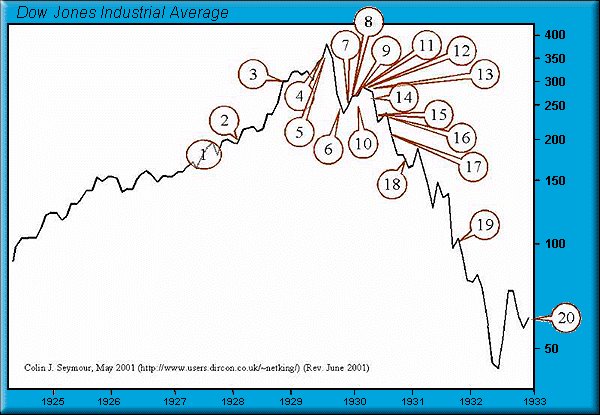

This blog “The Depression of 2006” gets a suggestion now and then to change the year until "I get it right." The year picked might not seem like much, but is important. It leaves room for perspective. Everyone can remember the 1929 depression from history class. The fact overlooked by the history books is that no one in 1929 thought they were even in a recession. Prosperity had reached a permanent plateau. The economic machine had been fine tuned and there would be no more economic dips. The word recession had not been invented. Technology had blossomed. New to this generation were, the telephone, the car, electric lights, the airplane and indoor plumbing. It wasn't until 1931 that everyone knew they were in a depression.

Here we are in 2007. Two weeks ago there was a 10% chance of a recession, now this week it’s more like 50%. Do you get the idea that a recession is only something you can see from the rear view mirror? The government will never make the call that a recession is in our midst. They have to deny it at all cost. Otherwise it could become a self feeding downward spiral.

Right now we have governors running around trying to save over leveraged home owners. This is really hard to figure out. The homeowner today can walk away from a home and probably not even have to consider bankruptcy. Get them to stay in that “home” an extra two years and enjoy the 200K drop in value. That’s an even worse mess. In six months we have progressed from “Canaries in coal mines” to “Horses and barn doors.” To top it off, the politicians are getting ready to pass laws to protect the homeowner from being looted ever again. There is nothing your politician can do to stop people from doing stupid things, that’s how they got elected in the first place!

We have a stock market that’s down 200, up 400, down 200. If you had a car that ran like that, your nose would be broken from hitting the windshield repeatedly. This is what you could label a bear market. Burn the Shorts until they fade away and then it is down we go forever (it will seem like that unless you're under 30 and have some time to burn until retirement).

Now we hear that a Florida State investment pool has suspended withdrawals. They had 27 billion two weeks ago and now have 18 billion, with 3 billion drawn out yesterday. This is where the cities, counties and school districts parked their spare cash before payday to earn a little more. The question comes up, will the teachers be paid this payday? We’re lucky that that didn’t happen in Kalifornia (methinks I should keep quiet). For the short bus crowd, this is a run on the bank. The SIV bailout or the homeowner refi, was going to be done with OPM (other people’s money). Now everyone wants to take the “my money” out of OPM.

So we have “The depression of 2006”, it’s just like 1929. Let’s see, add three years, and that would make 2009 as the year to watch. You will know then that you have arrived. The only damn problem is, no one wanted to take the trip. Talk about ingratitude, the depression of a life time, what an experience! No ticket needed, front row seats for everyone. And you thought you needed a travel agent!

Here we are in 2007. Two weeks ago there was a 10% chance of a recession, now this week it’s more like 50%. Do you get the idea that a recession is only something you can see from the rear view mirror? The government will never make the call that a recession is in our midst. They have to deny it at all cost. Otherwise it could become a self feeding downward spiral.

Right now we have governors running around trying to save over leveraged home owners. This is really hard to figure out. The homeowner today can walk away from a home and probably not even have to consider bankruptcy. Get them to stay in that “home” an extra two years and enjoy the 200K drop in value. That’s an even worse mess. In six months we have progressed from “Canaries in coal mines” to “Horses and barn doors.” To top it off, the politicians are getting ready to pass laws to protect the homeowner from being looted ever again. There is nothing your politician can do to stop people from doing stupid things, that’s how they got elected in the first place!

We have a stock market that’s down 200, up 400, down 200. If you had a car that ran like that, your nose would be broken from hitting the windshield repeatedly. This is what you could label a bear market. Burn the Shorts until they fade away and then it is down we go forever (it will seem like that unless you're under 30 and have some time to burn until retirement).

Now we hear that a Florida State investment pool has suspended withdrawals. They had 27 billion two weeks ago and now have 18 billion, with 3 billion drawn out yesterday. This is where the cities, counties and school districts parked their spare cash before payday to earn a little more. The question comes up, will the teachers be paid this payday? We’re lucky that that didn’t happen in Kalifornia (methinks I should keep quiet). For the short bus crowd, this is a run on the bank. The SIV bailout or the homeowner refi, was going to be done with OPM (other people’s money). Now everyone wants to take the “my money” out of OPM.

So we have “The depression of 2006”, it’s just like 1929. Let’s see, add three years, and that would make 2009 as the year to watch. You will know then that you have arrived. The only damn problem is, no one wanted to take the trip. Talk about ingratitude, the depression of a life time, what an experience! No ticket needed, front row seats for everyone. And you thought you needed a travel agent!

Saturday, November 24, 2007

Bernanke, the Sheep Herder

Through the ages we have had Sages that could read the future from animal entrails. Bernanke does a pretty good job at this, it’s an acquired skill, learn as you go, and go with the flow. If you are not sure, be vague.

There is only one problem. Things are beginning to go wrong and Bernanke is being blamed. That doesn’t make much sense. His interpretation of goat entrails or what ever, is a defined process and hasn’t changed much. The joke is the suggestion that this guy even belongs in the loop. As long as economy was running OK, there was no problem, his wisdom was unquestioned. Now, that things are off course, Bernanke seems to be the guy that could have saved us, if he had only read the entrails correctly.

Today’s new stock trader has been brought up on the idea of the Feds are in control. These "couch experts" are afraid to even question that premise for fear of appearing uneducated or over medicated. You hear a statement that the Feds are pumping liquidity to the banking system. Ask anyone jumping up and down, what that means, or who gets the money, they haven’t got a clue. The visual abstraction of pumping money into anything is kind of vague. You are left with the feeling that things are under control. The Feds supply the who, what, why, when and where, but you can’t drive there. Useless information that's suppose to mean something to everyone!

It’s kind of like your daughter going out on a date, and you ask what they did. The reply, “We went to the movies.” That’s all fine and dandy, until the hotel calls up and says they forgot to pay for the porn movie rental. In this case, the "pumping" is more a visual than an abstraction.

The dollar is dropping in value, and the interest rate on T-bills is decreasing. This is the equivalent of losing your brakes and steering while driving down a mountain pass (minor problem). As the dollar depreciates against foreign currencies, foreign capital leaves the country. Interest rates have to rise to attract capital back. Interest rates won't be attractive to foreigners if the dollar is dropping like a Bear Sterns CDO (the new Confederate Dollar). The odd thing is that "scared money" wants to be in T-bills for security. This is driving rates down. The expected reaction, of interest rates rising, isn't happening. This has to be big. Banks only insure 100K. T-bills insure every depositer. A rich man doesn’t have to stop at 600 banks to insure 60 million. T-bills are the McDonald's equivalent of a drive thru; fast bank insurance, for the super rich.

The only thing that can be deduced from the market right now, is that Economics 101 is not functioning as expected. Business models are falling apart. The estimates as to how bad things are, have doubled in size in the span of three months.

All of this money that has been lost, it doesn’t belong to anyone. It kind of makes you wonder if Bernanke and Company are rewriting our fairy tales for Christmas. Put some "Christmas Cheer" in your tank while you drive your Hummer to the Poor House, stop by Star-sawbucks and order up a "Bernanke Latte" (Ethanol, no cream).

There is only one problem. Things are beginning to go wrong and Bernanke is being blamed. That doesn’t make much sense. His interpretation of goat entrails or what ever, is a defined process and hasn’t changed much. The joke is the suggestion that this guy even belongs in the loop. As long as economy was running OK, there was no problem, his wisdom was unquestioned. Now, that things are off course, Bernanke seems to be the guy that could have saved us, if he had only read the entrails correctly.

Today’s new stock trader has been brought up on the idea of the Feds are in control. These "couch experts" are afraid to even question that premise for fear of appearing uneducated or over medicated. You hear a statement that the Feds are pumping liquidity to the banking system. Ask anyone jumping up and down, what that means, or who gets the money, they haven’t got a clue. The visual abstraction of pumping money into anything is kind of vague. You are left with the feeling that things are under control. The Feds supply the who, what, why, when and where, but you can’t drive there. Useless information that's suppose to mean something to everyone!

It’s kind of like your daughter going out on a date, and you ask what they did. The reply, “We went to the movies.” That’s all fine and dandy, until the hotel calls up and says they forgot to pay for the porn movie rental. In this case, the "pumping" is more a visual than an abstraction.

The dollar is dropping in value, and the interest rate on T-bills is decreasing. This is the equivalent of losing your brakes and steering while driving down a mountain pass (minor problem). As the dollar depreciates against foreign currencies, foreign capital leaves the country. Interest rates have to rise to attract capital back. Interest rates won't be attractive to foreigners if the dollar is dropping like a Bear Sterns CDO (the new Confederate Dollar). The odd thing is that "scared money" wants to be in T-bills for security. This is driving rates down. The expected reaction, of interest rates rising, isn't happening. This has to be big. Banks only insure 100K. T-bills insure every depositer. A rich man doesn’t have to stop at 600 banks to insure 60 million. T-bills are the McDonald's equivalent of a drive thru; fast bank insurance, for the super rich.

The only thing that can be deduced from the market right now, is that Economics 101 is not functioning as expected. Business models are falling apart. The estimates as to how bad things are, have doubled in size in the span of three months.

All of this money that has been lost, it doesn’t belong to anyone. It kind of makes you wonder if Bernanke and Company are rewriting our fairy tales for Christmas. Put some "Christmas Cheer" in your tank while you drive your Hummer to the Poor House, stop by Star-sawbucks and order up a "Bernanke Latte" (Ethanol, no cream).

Saturday, November 17, 2007

Deutsche Bank's View on the Housing Crisis

Here is part of an article "The Subprime Mortgage Crisis and its Wake," dated November 15, 2007, that was emailed to me by a reader. It discusses the present housing crisis and appears to have been put out by Deutsche Bank. I'm not sure if this was meant for public consumption. It seems legit.The bank has been accused of being one of the biggest homeowners (by way of foreclosure) in the U. S.

Page 6 displays their view of the future housing problem.

Double click for larger picture. Source: Deutsche Bank.

Page 28 lists the CDO and SIV exposure for banks in US and Europe. Where is Asia????

Double click for larger picture. Source: Deutsche Bank.

It does seem to confirm my contention that the banks know pretty well what's happening three months from now, right now.

Page 6 displays their view of the future housing problem.

Double click for larger picture. Source: Deutsche Bank.

Page 28 lists the CDO and SIV exposure for banks in US and Europe. Where is Asia????

Double click for larger picture. Source: Deutsche Bank.

It does seem to confirm my contention that the banks know pretty well what's happening three months from now, right now.

Thursday, November 15, 2007

Pipe Dream Bankers

Let’s see it was July and all was well, and then Bear Sterns had two hedge funds go poof. Financial funding for housing dropped dead. Now three months later you read the headline “Bear Stearns Says Worst Is Over After Writedown”. Seems as if the damaged has been contained.

The housing foreclosure rate during the present one year period has exceeded what took three years, the last time these values were reached. The sub prime resets are just beginning. We have Bear Sterns with no problem four months ago now saying that the worst is over. I submit that what we know today they knew three months ago. So to fast forward three months from now, Bear Sterns as well as the rest of the crowd could be going parabolic on losses. What they know now, we won’t read about, until January rolls around (keep quiet keep your job).

Then to top this off, Citigroup, Bank of America and JPMorgan Chase (the Larry, Moe and Curly of finance), have formed a triumvirate to bail out the SIV’s with a 100 billion dollar fund. Where do you get money like that for such a lost cause? (I can think of two sources, Visa and Master Card) It’s kind of like a hooker with VD. You get a great rate today, but you pay later (it gives new meaning to “Share what you have”).

100 Billion, that's more than 5 General Motors Corporations. Where do you get that much money from? It's a little like the joke about the psychiatrist examining a patient who asks "What would you do if a tank came rolling toward you?" the Patient say "I'd hop in my Porsche and drive away." The shrink says "Where did you get the Porsche?" The patient says, "The same place you got the tank."

The only problem I see, is that this might not be Monopoly money when they begin the program, but it could live "up" to our expectations, given time.

The housing foreclosure rate during the present one year period has exceeded what took three years, the last time these values were reached. The sub prime resets are just beginning. We have Bear Sterns with no problem four months ago now saying that the worst is over. I submit that what we know today they knew three months ago. So to fast forward three months from now, Bear Sterns as well as the rest of the crowd could be going parabolic on losses. What they know now, we won’t read about, until January rolls around (keep quiet keep your job).

Then to top this off, Citigroup, Bank of America and JPMorgan Chase (the Larry, Moe and Curly of finance), have formed a triumvirate to bail out the SIV’s with a 100 billion dollar fund. Where do you get money like that for such a lost cause? (I can think of two sources, Visa and Master Card) It’s kind of like a hooker with VD. You get a great rate today, but you pay later (it gives new meaning to “Share what you have”).

100 Billion, that's more than 5 General Motors Corporations. Where do you get that much money from? It's a little like the joke about the psychiatrist examining a patient who asks "What would you do if a tank came rolling toward you?" the Patient say "I'd hop in my Porsche and drive away." The shrink says "Where did you get the Porsche?" The patient says, "The same place you got the tank."

The only problem I see, is that this might not be Monopoly money when they begin the program, but it could live "up" to our expectations, given time.

Sunday, November 11, 2007

Rose Colored Glasses

The dollar index has dropped from 120 to 75.Doesn’t seem possible does it? No big Presidential announcement like when Nixon devalued the dollar. No wonder Gold, Silver and Oil jumped in price. I’m sure Congress will “Round up the usual suspects.” It’s your regular Bogart movie run amuck staring Bernanke and Greenspan. It has a lot to do with the money we borrowed from other countries.

Japan holds 586 billion in T-bills and China the second biggest holder has 400 billion. The United Kingdom is third with 244 billion. If you add up all the other countries holding our paper it comes to a grand total of 2.231 trillion dollars. The good thing about all of this, it’s not our problem (it’s not our money). The bad thing is we spent it!

Foreigners have “invested” 2 trillion in T-bills. Our banks are holding 1 trillion in credit card debt and maybe another 2 trillion in USA’s (Up in Smoke Assets). And then there is the Social Security Trust Fund (another USA IOU). On the plus side, the stock market was worth 15 trillion dollars last week. Hamburger could be on sale next week (bull burgers).

The 5 year T-bond is trading at 3.75%, the Fed funds are at 4.5% and inflation is roaring in at 4% to 10% (choose your own value, I’m easy). One article suggested that the 2 trillion dollar foreign investment in Treasuries has shaved about a percentage point off of our T-bill rate. That alone indicates to me that not everyone on steroids is in sports.

So much good news is floating around; the housing disaster seems to have disappeared, the CDO’s are water under the bridge. It seems as if everything is under control, we have decided to live with $100 a barrel oil. I guess that it is the current lack of bad news that makes the financial picture seem so rosy. It’s amazing how, given a little time, we adjust to our new environment and carry on with life.

Just don't try reading your latest 401K quarterly report over dinner. You're going to choke!

Japan holds 586 billion in T-bills and China the second biggest holder has 400 billion. The United Kingdom is third with 244 billion. If you add up all the other countries holding our paper it comes to a grand total of 2.231 trillion dollars. The good thing about all of this, it’s not our problem (it’s not our money). The bad thing is we spent it!

Foreigners have “invested” 2 trillion in T-bills. Our banks are holding 1 trillion in credit card debt and maybe another 2 trillion in USA’s (Up in Smoke Assets). And then there is the Social Security Trust Fund (another USA IOU). On the plus side, the stock market was worth 15 trillion dollars last week. Hamburger could be on sale next week (bull burgers).

The 5 year T-bond is trading at 3.75%, the Fed funds are at 4.5% and inflation is roaring in at 4% to 10% (choose your own value, I’m easy). One article suggested that the 2 trillion dollar foreign investment in Treasuries has shaved about a percentage point off of our T-bill rate. That alone indicates to me that not everyone on steroids is in sports.

So much good news is floating around; the housing disaster seems to have disappeared, the CDO’s are water under the bridge. It seems as if everything is under control, we have decided to live with $100 a barrel oil. I guess that it is the current lack of bad news that makes the financial picture seem so rosy. It’s amazing how, given a little time, we adjust to our new environment and carry on with life.

Just don't try reading your latest 401K quarterly report over dinner. You're going to choke!

Sunday, November 04, 2007

Money From Nowhere Going Somewhere

Private industry and government both contribute to the economy. An economist uses a rule of thumb that private investment has a 5 to 1 multiplier effect on the economy; whereas government expenditures contribute at a 2 to 1 ratio. So, to stimulate the economy, private investment is the most cost effective and transfer payments the least.

Here is where I get shot for simplification again. Divide the government into five areas of financial involvement; administration, infrastructure, defense, education and retirement.

Administrative tasks produce nothing and could be considered transfer payments. It comes from our taxes and goes into a paycheck (government, police, fire etc).

Infrastructure and defense purchases by government create jobs where something is produced for the economy. Congress spends billions dollars on the Iraq war. The money is not shipped off to Iraq. Private companies build new war machinery. This mirrors private investment returns at a somewhat lower scale.

Education is kind of a necessary lubricant for the whole system. It has returns that benefit the economy; they are not as visible. When a sales clerk can’t make change for a $20 bill, the need for education becomes very apparent.

Retirement and government health care are also transfer payments. Our tax dollars go into a retiree's bank account. This stimulates consumption but no new product was added to the economy. I know someone will say, “Hey that Social Security money is mine, I paid into the system.” How about if we cut your benefits off when you exceed what you contributed? The fact is some guy, who died after 35 years on social security, probably consumed all of your contributions and ten other people’s as well.

So let’s go one step further. Home equity loan withdrawals are another form of transfer payments. Notice, the money extracted from mortgage equity withdrawals (MEW) was not earned by building something new for the economy. Housing just doubled in price; it’s free money (this is the way the government does it). Of course, the homeowner is supposed to pay it back. It looks as if that concept has a “few” holes in it.

Step back and look at the big picture. Government can issue checks for retirement and health care costs by increasing the national debt. This is what the homeowner was doing with a MEW. The American consumer has been on a buying binge with US monopoly money. Where did all of this stuff that we didn’t make but we needed to purchase come from? Here's a clue “lead paint.”

Looks like this Thanksgiving, we are giving China the bird. Just maybe they will give us a goose for Christmas (triple pun intended).

Here is where I get shot for simplification again. Divide the government into five areas of financial involvement; administration, infrastructure, defense, education and retirement.

Administrative tasks produce nothing and could be considered transfer payments. It comes from our taxes and goes into a paycheck (government, police, fire etc).

Infrastructure and defense purchases by government create jobs where something is produced for the economy. Congress spends billions dollars on the Iraq war. The money is not shipped off to Iraq. Private companies build new war machinery. This mirrors private investment returns at a somewhat lower scale.

Education is kind of a necessary lubricant for the whole system. It has returns that benefit the economy; they are not as visible. When a sales clerk can’t make change for a $20 bill, the need for education becomes very apparent.

Retirement and government health care are also transfer payments. Our tax dollars go into a retiree's bank account. This stimulates consumption but no new product was added to the economy. I know someone will say, “Hey that Social Security money is mine, I paid into the system.” How about if we cut your benefits off when you exceed what you contributed? The fact is some guy, who died after 35 years on social security, probably consumed all of your contributions and ten other people’s as well.

So let’s go one step further. Home equity loan withdrawals are another form of transfer payments. Notice, the money extracted from mortgage equity withdrawals (MEW) was not earned by building something new for the economy. Housing just doubled in price; it’s free money (this is the way the government does it). Of course, the homeowner is supposed to pay it back. It looks as if that concept has a “few” holes in it.

Step back and look at the big picture. Government can issue checks for retirement and health care costs by increasing the national debt. This is what the homeowner was doing with a MEW. The American consumer has been on a buying binge with US monopoly money. Where did all of this stuff that we didn’t make but we needed to purchase come from? Here's a clue “lead paint.”

Looks like this Thanksgiving, we are giving China the bird. Just maybe they will give us a goose for Christmas (triple pun intended).

Tuesday, October 30, 2007

Jim Roger's Opinion of Helicopter Ben

Here is a seven minute video on Jim Rogers reflecting on the Grand Wizard Ben Bernanke. It's worth viewing. Notice when he says that housing is in more than a recession that suggests things are a lot more dicey than most people believe. The bottom to the RE market is a while away, so it gives one chance to ponder the effects of the next rate cut scheduled for tomorrow. Unfortunatly, IMHO, the last thing we need is a rate cut. Click here to view the video.

Sunday, October 28, 2007

N Y Stock Exchange Changes the Rules

Bloomberg reported Friday that the NYSE eliminated computer trading curbs when the market goes up or down drastically. Last December the exchange completed their conversion over to electronic trading. Then in July, they got rid of the uptick rule which prevented the shorts from piling on in a down market. The training wheels are off.

With all of the computer trading going on, things could get a bit wild. Each Mutual fund, pension plan, IRA etc, probably has a program that will instantaneously calculate and execute arbitrage positions to take advantage of the current market. What we may be looking at is an electronic financial war, your retirement fund against mine.

The computer programming used by the NYSE has been pretty well tested in an up market, but it has never really been tested in a down market. It’s a little like the housing market. No problem going up.

Suppose someone types in a sell order with too many zeros in it by mistake and hits enter. White out isn’t going to fix it. By the time someone says oops, we could have a meltdown. If the herd (seasoned money managers) panics, it’s going to be over fast (speed of light comes to mind). It’s kind of like having a party where you use dynamite sticks for birthday candles; everyone's going to remember that special occasion for all the wrong reasons.

With all of the computer trading going on, things could get a bit wild. Each Mutual fund, pension plan, IRA etc, probably has a program that will instantaneously calculate and execute arbitrage positions to take advantage of the current market. What we may be looking at is an electronic financial war, your retirement fund against mine.

The computer programming used by the NYSE has been pretty well tested in an up market, but it has never really been tested in a down market. It’s a little like the housing market. No problem going up.

Suppose someone types in a sell order with too many zeros in it by mistake and hits enter. White out isn’t going to fix it. By the time someone says oops, we could have a meltdown. If the herd (seasoned money managers) panics, it’s going to be over fast (speed of light comes to mind). It’s kind of like having a party where you use dynamite sticks for birthday candles; everyone's going to remember that special occasion for all the wrong reasons.

Saturday, October 27, 2007

Perception: Your Point of View Verses Mine- reprinted

This is reprinted from July 15 2006. It may help you look at the world a little differently. I have to examine this issue every time I publish.

After cruising a lot of blogs, I've noticed something that I wasn't really aware of. Ever notice that after you buy that new car, you seem to spot a lot of them on the highway, whereas before the purchase you didn't? The thing that I noticed was, the fact that our minds are sharpened to recognize stimulus that we accept into the model of our perceived world.

The real estate bubble bloggers, see the real estate market falling off of a cliff. The real estate agent sees a return to a more normal market. It's not really a matter of who is right, but rather one of timing. Real Estate has been trying to fall off of that cliff for several years, and yet some real estate agents are making a decent living.

I do believe in the example I have cited with real estate, it will fall off a cliff. The "when" part I am not sure about. What needs to be pointed out is that what you expect to happen, colors how you perceive the markets. It's kind of like the cartoon of two men on a very small island. One puts oar locks to the left and right and puts in two oars and starts to row to the west, the other guy on the island throws his hands up and says "you're rowing the wrong way!"

What needs to be realized is that what we want or expect to see, is far more observable than that what we care little about. Captain Ahab harpooning the great white whale nailed the whale, but the rope was wrapped around his leg--he didn't see it coming.

Our faulty perception of the world can harm us. Real estate could be collapsing and you laugh at the guy that looses his house. With 100% financing, don't laugh at him he's home free. It's the bank that gets hung. And when you trace it back far enough; your retirement fund probably took the big hit.

My point is, you will see what you want to see.

From here, we might just question more critically our observations of the world about us. Reality for the individual is all about perceived perception. It is real and different for each individual. To the group, it may not be. Hence the reality, "I could be wrong!"

It sure feels nice not to have to be right all of the time!

After cruising a lot of blogs, I've noticed something that I wasn't really aware of. Ever notice that after you buy that new car, you seem to spot a lot of them on the highway, whereas before the purchase you didn't? The thing that I noticed was, the fact that our minds are sharpened to recognize stimulus that we accept into the model of our perceived world.

The real estate bubble bloggers, see the real estate market falling off of a cliff. The real estate agent sees a return to a more normal market. It's not really a matter of who is right, but rather one of timing. Real Estate has been trying to fall off of that cliff for several years, and yet some real estate agents are making a decent living.

I do believe in the example I have cited with real estate, it will fall off a cliff. The "when" part I am not sure about. What needs to be pointed out is that what you expect to happen, colors how you perceive the markets. It's kind of like the cartoon of two men on a very small island. One puts oar locks to the left and right and puts in two oars and starts to row to the west, the other guy on the island throws his hands up and says "you're rowing the wrong way!"

What needs to be realized is that what we want or expect to see, is far more observable than that what we care little about. Captain Ahab harpooning the great white whale nailed the whale, but the rope was wrapped around his leg--he didn't see it coming.

Our faulty perception of the world can harm us. Real estate could be collapsing and you laugh at the guy that looses his house. With 100% financing, don't laugh at him he's home free. It's the bank that gets hung. And when you trace it back far enough; your retirement fund probably took the big hit.

My point is, you will see what you want to see.

From here, we might just question more critically our observations of the world about us. Reality for the individual is all about perceived perception. It is real and different for each individual. To the group, it may not be. Hence the reality, "I could be wrong!"

It sure feels nice not to have to be right all of the time!

Friday, October 26, 2007

The Solution is Too Simple

Just listening to CNBC again. Some ethanol producer was stating that ethanol production will save the importing of 480 million barrels of oil. The logic sounds great, but what if you were told that it takes more than a gallon of gasoline to produce a half gallon of ethanol. Here is a link to some hard facts. Why don’t we just stop growing corn for ethanol production? That ought to save about 960 million barrels (using his figures).

Why feed cattle? A farmer can make more money planting corn for ethanol production. It gets worse; the price of ethanol has all sorts of government subsidies. There is money to be made. Congressmen are hanging all over this one. They will save America from high priced oil. Notice that no one has ever accused a Congressman of being intelligent (you know they would deny it). But being crafty is a different story.

If everyone decided to take two steps backwards for every step taken forward, we would all be walking backwards to get to our destination. It just goes to prove that economics and common sense don’t mix. The economics floats to the top.

The real neat thing is that you pay more for less and feel good about it.

Why feed cattle? A farmer can make more money planting corn for ethanol production. It gets worse; the price of ethanol has all sorts of government subsidies. There is money to be made. Congressmen are hanging all over this one. They will save America from high priced oil. Notice that no one has ever accused a Congressman of being intelligent (you know they would deny it). But being crafty is a different story.

If everyone decided to take two steps backwards for every step taken forward, we would all be walking backwards to get to our destination. It just goes to prove that economics and common sense don’t mix. The economics floats to the top.

The real neat thing is that you pay more for less and feel good about it.

Thursday, October 25, 2007

The Recession has been canceled

Just finished watching the CNBC interview with the Presidents economic team. After viewing that, I think that its time to seriously start shorting fertilizer futures. The good news is that there isn’t going to be a recession. The bad news is that only one or two economists has ever predicted a recession and been correct.

They claimed the employment figures were good and production was up. What do we produce besides drywall? Everything in our home that we have bought in the last five years has a label with the words “Made in China.” Of course food items don’t count but we do still produce most of them. Instead of stuffing corn in cows, we are making ethanol to put in your car. Your t-bone steak went to $10 a pound so you could corrode the hell out of your fuel lines, go figure!

The funny thing is, if the President’s economic team was to predict a recession, no one would believe them, just as they don’t now.

Housing literally walked into an open manhole. The increase in oil prices is the new Arab income tax. And the financial community claims that the smoke is necessary with all the mirrors they are using.

One of the group, Mr. Hubbard, also stated that inflation was “very, very low.” Here is a link to the interview transcript.

So I’m glad that's out of the way, there will be no recession. The Presidential "Sages" have spoken.

They claimed the employment figures were good and production was up. What do we produce besides drywall? Everything in our home that we have bought in the last five years has a label with the words “Made in China.” Of course food items don’t count but we do still produce most of them. Instead of stuffing corn in cows, we are making ethanol to put in your car. Your t-bone steak went to $10 a pound so you could corrode the hell out of your fuel lines, go figure!

The funny thing is, if the President’s economic team was to predict a recession, no one would believe them, just as they don’t now.

Housing literally walked into an open manhole. The increase in oil prices is the new Arab income tax. And the financial community claims that the smoke is necessary with all the mirrors they are using.

One of the group, Mr. Hubbard, also stated that inflation was “very, very low.” Here is a link to the interview transcript.

So I’m glad that's out of the way, there will be no recession. The Presidential "Sages" have spoken.

Tuesday, October 23, 2007

Google, Absurdum

I figured that we ought to touch on some real “bat guano” here for a bit. Google has gone hyperbolic and it is reminiscent of another stock back in the last big melt down.

RCA started off in the stock market in 1921 at $1.50 a share and in 1929 rose up to $549 (if you don’t figure in the 4 for 1 split in 1929). Remember that back then Joe Six-NO-pack (prohibition) paid about $15 per month rent. 549 bucks was a hell of a lot of money. RCA did not pay a dividend (you don’t need one with that sort of performance).

Fast forward to today and we look at Google the "Wunderkind" of the stocks market. If we carry the comparison back to 1929, a Model T ford was $400 so you are looking for a Beamer or better in today's market. That would be a stock price of about $28,000 a share. I guess we are not there yet. The peculiar thing about the Google graph is that the scale is extremely misleading. If you reversed the horizontal and vertical perspectives, it would look like the first graph. (Graph courtesy of MoneyCentral.MSN.com)

The RCA visual aid also includes another bubble stock called AOL. They bought out Time Warner in 2000. What happened next to Time Warner could be best described as having to do with two well known products Astroglide and Preparation H. That affair pretty much ended after the star crossed lovers meld hit $15 on the stock exchange. Time Warner reassumed its "maiden name" and has AOL stuffed in a closet somewhere.

History describes how Sir Isaac Newton made a bundle on The South Sea Company in the 1620's only to reinvest back and lose it all. Even a year ago Google looked dicey. Here is a link to Googleiots an article from this blog a year ago (nothing much has changed).

When you add up what the company does and how easily it could be replaced for 1/20th of its market cap, its price is absurd. Nobody laughed when AOL bought Time Warner (and nobody has laughed about it since then either).

Maybe Cramer has a prediction for Google to hit $1000. Are we rich yet?

Sunday, October 21, 2007

Economic Turpitude

Banks, hedge funds and what ever are taking billions of dollars in loan loss provisions. I have been suggesting for over a year, that a lot of this money may be coming from our retirement funds. Think about it. If your wife buys a new fur coat with your paycheck, now you can’t pay the rent, that is obvious very fast. If the wife turned a trick with the old geezer down stairs and bought the coat, you are stuck wondering how she did it. The reason I suggest Retirement funds, is that the losses suffered so far appear to affect no one. But bear in mind, retirement income funds deal with the future. Most people are not ready to retire so these funds should have plenty of time to recover losses (keep quiet, keep your job). The write downs are massive. Nobody even blinks an eye. What’s a 10 billion dollar loss? The perspective is beyond comprehension. This money has to be coming from somewhere. Whoever’s money it is, they don’t seem to need it--yet.

The money supply worldwide seems to be contracting. Usually this would imply a rise in interest rates. That doesn’t seem to be happening. Commodities are increasing in value, which could be an inflation indicator. If reserves are being added to the banking system, then this could explain why rates are not rising (using a truck is cheaper than using Ben's helicopter).

A lot of the new earned money entering into the economy is not being used to create new jobs, its being “invested” in financial instruments. Workers are not creating new product, investors are placing side bets on the financial markets. The profit is gone from home building industry. Investment in rental property is a losing enterprise. Consumption seems to be tapering off. Home remodeling appears to have hit the skids. Starbucks seems to be doing OK, you have to draw the line somewhere.

Interest rates are dropping but you can't force people to borrow money unless there is some sort of return (like a house appreciating at 20% a year). That would explain why the stock market as well as the commodity’s markets are still in play. Cramer the other night was forecasting Google at $750. Everything is still going up. The stock market had a little hiccup on Friday. Nothing to worry about, Google kept on ticking just like a Timex watch. Of course it can’t be a bubble, bubbles don’t get that big!

You have a bunch of banks forming a consortium to bail out the CDO and SIV holders . They are creating a new financial instrument called a "USA," which is short for “Up in Smoke Assets.” It ought to be a hot item if they can figure out a way to package it. It’s kind of like selling invisible goldfish. Give the buyer one or two extra for free, so he thinks he’s getting a real bargain and sell him some invisible fish food to boot.

The economy’s current condition reminds me of the embezzler and a millionaire taking a vacation at the same resort. The embezzler knows whose money he is spending. The millionaire has no idea that he is broke, but hey, everyone is having fun. Are we broke yet?

The money supply worldwide seems to be contracting. Usually this would imply a rise in interest rates. That doesn’t seem to be happening. Commodities are increasing in value, which could be an inflation indicator. If reserves are being added to the banking system, then this could explain why rates are not rising (using a truck is cheaper than using Ben's helicopter).

A lot of the new earned money entering into the economy is not being used to create new jobs, its being “invested” in financial instruments. Workers are not creating new product, investors are placing side bets on the financial markets. The profit is gone from home building industry. Investment in rental property is a losing enterprise. Consumption seems to be tapering off. Home remodeling appears to have hit the skids. Starbucks seems to be doing OK, you have to draw the line somewhere.

Interest rates are dropping but you can't force people to borrow money unless there is some sort of return (like a house appreciating at 20% a year). That would explain why the stock market as well as the commodity’s markets are still in play. Cramer the other night was forecasting Google at $750. Everything is still going up. The stock market had a little hiccup on Friday. Nothing to worry about, Google kept on ticking just like a Timex watch. Of course it can’t be a bubble, bubbles don’t get that big!

You have a bunch of banks forming a consortium to bail out the CDO and SIV holders . They are creating a new financial instrument called a "USA," which is short for “Up in Smoke Assets.” It ought to be a hot item if they can figure out a way to package it. It’s kind of like selling invisible goldfish. Give the buyer one or two extra for free, so he thinks he’s getting a real bargain and sell him some invisible fish food to boot.

The economy’s current condition reminds me of the embezzler and a millionaire taking a vacation at the same resort. The embezzler knows whose money he is spending. The millionaire has no idea that he is broke, but hey, everyone is having fun. Are we broke yet?

Monday, October 15, 2007

Arbitrage, Free Money