Here is something that I ran across that seems like a parallel to todays mindset.

This is a link to the site: http://www.gold-eagle.com/editorials_01/seymour062001.html

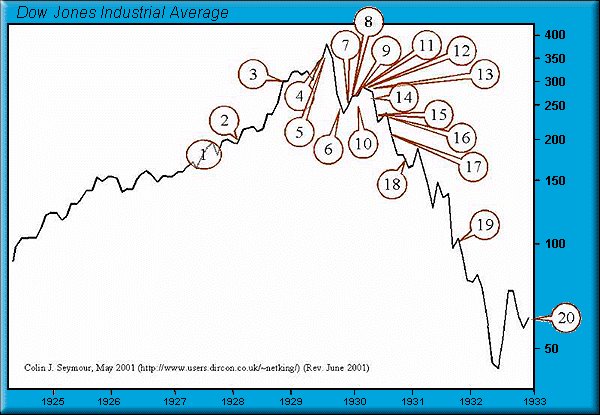

Begin Copied Material:1927-1933 Chart of Pompous Prognosticators

1. "We will not have any more crashes in our time."

- John Maynard Keynes in 1927

2. "I cannot help but raise a dissenting voice to statements that we are living in a fool's paradise, and that prosperity in this country must necessarily diminish and recede in the near future."

- E. H. H. Simmons, President, New York Stock Exchange, January 12, 1928

"There will be no interruption of our permanent prosperity."

- Myron E. Forbes, President, Pierce Arrow Motor Car Co., January 12, 1928

3. "No Congress of the United States ever assembled, on surveying the state of the Union, has met with a more pleasing prospect than that which appears at the present time. In the domestic field there is tranquility and contentment...and the highest record of years of prosperity. In the foreign field there is peace, the goodwill which comes from mutual understanding."

- Calvin Coolidge December 4, 1928

4. "There may be a recession in stock prices, but not anything in the nature of a crash."

- Irving Fisher, leading U.S. economist , New York Times, Sept. 5, 1929

5. "Stock prices have reached what looks like a permanently high plateau. I do not feel there will be soon if ever a 50 or 60 point break from present levels, such as (bears) have predicted. I expect to see the stock market a good deal higher within a few months."

- Irving Fisher, Ph.D. in economics, Oct. 17, 1929

"This crash is not going to have much effect on business."

- Arthur Reynolds, Chairman of Continental Illinois Bank of Chicago, October 24, 1929

"There will be no repetition of the break of yesterday... I have no fear of another comparable decline."

- Arthur W. Loasby (President of the Equitable Trust Company), quoted in NYT, Friday, October 25, 1929

"We feel that fundamentally Wall Street is sound, and that for people who can afford to pay for them outright, good stocks are cheap at these prices."

- Goodbody and Company market-letter quoted in The New York Times, Friday, October 25, 1929

6. "This is the time to buy stocks. This is the time to recall the words of the late J. P. Morgan... that any man who is bearish on America will go broke. Within a few days there is likely to be a bear panic rather than a bull panic. Many of the low prices as a result of this hysterical selling are not likely to be reached again in many years."

- R. W. McNeel, market analyst, as quoted in the New York Herald Tribune, October 30, 1929

"Buying of sound, seasoned issues now will not be regretted"

- E. A. Pearce market letter quoted in the New York Herald Tribune, October 30, 1929

"Some pretty intelligent people are now buying stocks... Unless we are to have a panic -- which no one seriously believes, stocks have hit bottom."

- R. W. McNeal, financial analyst in October 1929

7. "The decline is in paper values, not in tangible goods and services...America is now in the eighth year of prosperity as commercially defined. The former great periods of prosperity in America averaged eleven years. On this basis we now have three more years to go before the tailspin."

- Stuart Chase (American economist and author), NY Herald Tribune, November 1, 1929

"Hysteria has now disappeared from Wall Street."

- The Times of London, November 2, 1929

"The Wall Street crash doesn't mean that there will be any general or serious business depression... For six years American business has been diverting a substantial part of its attention, its energies and its resources on the speculative game... Now that irrelevant, alien and hazardous adventure is over. Business has come home again, back to its job, providentially unscathed, sound in wind and limb, financially stronger than ever before."

- Business Week, November 2, 1929

"...despite its severity, we believe that the slump in stock prices will prove an intermediate movement and not the precursor of a business depression such as would entail prolonged further liquidation..."

- Harvard Economic Society (HES), November 2, 1929

8. "... a serious depression seems improbable; [we expect] recovery of business next spring, with further improvement in the fall."

- HES, November 10, 1929

"The end of the decline of the Stock Market will probably not be long, only a few more days at most."

- Irving Fisher, Professor of Economics at Yale University, November 14, 1929

"In most of the cities and towns of this country, this Wall Street panic will have no effect."

- Paul Block (President of the Block newspaper chain), editorial, November 15, 1929

"Financial storm definitely passed."

- Bernard Baruch, cablegram to Winston Churchill, November 15, 1929

9. "I see nothing in the present situation that is either menacing or warrants pessimism... I have every confidence that there will be a revival of activity in the spring, and that during this coming year the country will make steady progress."

- Andrew W. Mellon, U.S. Secretary of the Treasury December 31, 1929

"I am convinced that through these measures we have reestablished confidence."

- Herbert Hoover, December 1929

"[1930 will be] a splendid employment year."

- U.S. Dept. of Labor, New Year's Forecast, December 1929

10. "For the immediate future, at least, the outlook (stocks) is bright."

- Irving Fisher, Ph.D. in Economics, in early 1930

11. "...there are indications that the severest phase of the recession is over..."

- Harvard Economic Society (HES) Jan 18, 1930

12. "There is nothing in the situation to be disturbed about."

- Secretary of the Treasury Andrew Mellon, Feb 1930

13. "The spring of 1930 marks the end of a period of grave concern...American business is steadily coming back to a normal level of prosperity."

- Julius Barnes, head of Hoover's National Business Survey Conference, Mar 16, 1930

"... the outlook continues favorable..."

- HES Mar 29, 1930

14 "... the outlook is favorable..."

- HES Apr 19, 1930

15. "While the crash only took place six months ago, I am convinced we have now passed through the worst -- and with continued unity of effort we shall rapidly recover. There has been no significant bank or industrial failure. That danger, too, is safely behind us."

- Herbert Hoover, President of the United States, May 1, 1930

"...by May or June the spring recovery forecast in our letters of last December and November should clearly be apparent..."

- HES May 17, 1930

"Gentleman, you have come sixty days too late. The depression is over."

- Herbert Hoover, responding to a delegation requesting a public works program to help speed the recovery, June 1930

16. "... irregular and conflicting movements of business should soon give way to a sustained recovery..."

- HES June 28, 1930

17. "... the present depression has about spent its force..."

- HES, Aug 30, 1930

18. "We are now near the end of the declining phase of the depression."

- HES Nov 15, 1930

19. "Stabilization at [present] levels is clearly possible."

- HES Oct 31, 1931

20. "All safe deposit boxes in banks or financial institutions have been sealed... and may only be opened in the presence of an agent of the I.R.S."

- President F.D. Roosevelt, 1933

End Copied MaterialQuotes #5 and #8 are very famous remarks by Irving Fisher, who at the time was managing the Yale endowment funds. It didn't go well from there.

These were very intelligent people back in their time. Their thoughts on what would happen next were way off the mark. What was said, sounded good and was reassuring.

It leaves a lot of doubt about what you can take for granted in todays newspapers

Note, quote 20 refers to the fact that it became illegal to own gold as an American citizen. The government was making sure no one was holding out on them. You had to trade your gold in for currency. This was FDR's way of keeping everyone honest--government excluded.