Let's see the banks are paying 5 percent interest and our current inflation rate is around 4 percent. That gives us a ONE percent rate of return. That certainly isn't much incentive to save for a rainy day, especially if the inflation rate is higher than what the government states.

Interest rates are an indicator of money in the market looking for a borrower. The rates are high if there is a shortage of money to loan and low if nobody wants to borrow. Obviously the United States is floating in surplus bank funds. The Feds raised the interest rate 17 times and the 30 year bond hiccupped.

Another name for this surplus is DEBT.

Joe Six Pack bought the car, the plasma screen and put it on plastic. Let's say he's on the high side of 30k on his cards and he has no problem making the monthly payments. Here is where the bank can do the Fannie Mae routine.

(The following is pure conjecture on my part and could be way out in left field.)

The bank needs to reimburse the retail outlet in cash for the goods charged. Now bear in mind that the bank is getting 18% minimum on these loan amounts carried over 30 days. What better way to raise money than to package these borrowers like Fannie Mae does and sell them to some mutual fund. This way, everyone gets paid and the game can continue. It seems to me, if this was done right, the bank passes the bag to some other institution like a pension plan wanting 8 to 10 percent on their funds. These notes would be far from FDIC insured.

Everyone that needs to borrow is probably already maxed out and wouldn't qualify for more borrowing using a regular loan. But, if you're a bank, you give them a credit card. As long as the banks can issue credit cards, the game can continue. The minute that they stop issuing cards, the game would be over. The banks have monetized the debt and created a perpetual money machine. The more you charge the better it gets.

Bye for now from Left Field.

Sunday, September 24, 2006

Wednesday, September 20, 2006

The Amaranth Fiasco

Looks like the Amaranth hedge fund is in deeper than it looks. Yesterday their losses were less than 3 billion. Now with their sale to J P Morgan Chase & Co and the hedge fund Citadel Investments, it looks closer to SIX BILLION!

As quoted from the Wall Street Journal:

It gets stranger as you dig deeper.

As quoted from the San Diego Union Tribune:

Then an article on the same page of the Tribune:

Here is a link to a previous post of mine on derivatives

Invisible Derivatives Market

The thing that I have been stressing, is that a lot of the money chasing the big returns could be retirement funds. That's where the big money is. If I'm right, its truly a sad time for a lot of people, this could get worse real fast.

A thirty two year old guy at Amaranth in a span of one week lost over 3 to 5 billion dollars.

Do you know who your retirement fund is sleeping with?

Final score: Amaranth ruined, San Diego County retirement caught in a compromising position

Truly an Ex-Lax moment!

As quoted from the Wall Street Journal:

As part of the deal, J.P. Morgan and Citadel could receive in the neighborhood of $2 billion of collateral that Amaranth had posted as margin on its various trades,

It gets stranger as you dig deeper.

As quoted from the San Diego Union Tribune:

Amaranth severely restricts investors' ability to cash in their holdings. Investors only can withdraw money on the anniversary of their investment and then only with 90 days' notice. If they try to withdraw at any point outside that time frame, they face a 2.5 percent penalty.

Even more Draconian, if investors redeem more than 7.5 percent of the fund's assets, Amaranth can refuse further withdrawals.

Then an article on the same page of the Tribune:

County pension may have lost millions in fund

The crash of the Amaranth hedge fund could have sizable repercussions for San Diego County's retirement system, which invested $175 million with Anaranth just last year.

The county retirement fund's losses could be as much as $45 million . . .

The retirement association already has terminated its agreement with Amaranth and is recalling its investment.

Here is a link to a previous post of mine on derivatives

Invisible Derivatives Market

The thing that I have been stressing, is that a lot of the money chasing the big returns could be retirement funds. That's where the big money is. If I'm right, its truly a sad time for a lot of people, this could get worse real fast.

A thirty two year old guy at Amaranth in a span of one week lost over 3 to 5 billion dollars.

Do you know who your retirement fund is sleeping with?

Final score: Amaranth ruined, San Diego County retirement caught in a compromising position

Truly an Ex-Lax moment!

Tuesday, September 19, 2006

The Interest Rate Spike

If you read today's paper, one of the largest hedge funds, Amaranth, took a 35% hit to assets. to the tune of 3 billion dollars. It only took a week. Most nightmares occur while you're asleep, this one is not going away when you wake up in the morning. Amaranth is selling corporate bonds to raise the cash.

What we are looking at here is the smell of smoke and its liable to get worse. Consider this a trial run for a date set in the future. Imagine all of the real estate second trust deeds going to zero and you can see a lot of hedge funds that have "insured" these "fine investments," out in the market trying to raise cash.

Step back for a minute and remember that the Feds sell a thirty year bond that's paying about 5%. Also most people are fully invested in something, house, stock market, gold, bonds. So, there is no liquidity for quick investment if you hold these assets.

Now picture the hedge funds starting to fall apart. Their objective is to raise cash. Sell assets like bonds and stocks. They need cash. Who has cash when the call for cash is quite large? At this point, the interest rate rises only because there are too many bonds at 5% for sale. Nobody wants them at that interest rate. Considering the potential losses in the second trust deed market, interest rates could spike to 20%.

So if interest rates were to hit 20% you could buy 30 year Treasury's at 25 cents on the dollar. $100,000 Treasury bond paying 5% could be bought for $25,000 in the ensuing panic. Remember, you have to have access to cash money to buy.

The damage and destruction would be over in a matter of weeks. From there, the bond market could be back to normal. So if the interest rate dropped back down to 5% the bond you purchased for $25,000 would now be worth $100,000 ---- a chance to quadruple your savings.

Sound far fetched? History doesn't quite repeat itself. Are you ready for the ride? ---The ride that will be "different this time?"

Cash will be King. For how long is anyone's guess. Are you ready for it?

What we are looking at here is the smell of smoke and its liable to get worse. Consider this a trial run for a date set in the future. Imagine all of the real estate second trust deeds going to zero and you can see a lot of hedge funds that have "insured" these "fine investments," out in the market trying to raise cash.

Step back for a minute and remember that the Feds sell a thirty year bond that's paying about 5%. Also most people are fully invested in something, house, stock market, gold, bonds. So, there is no liquidity for quick investment if you hold these assets.

Now picture the hedge funds starting to fall apart. Their objective is to raise cash. Sell assets like bonds and stocks. They need cash. Who has cash when the call for cash is quite large? At this point, the interest rate rises only because there are too many bonds at 5% for sale. Nobody wants them at that interest rate. Considering the potential losses in the second trust deed market, interest rates could spike to 20%.

So if interest rates were to hit 20% you could buy 30 year Treasury's at 25 cents on the dollar. $100,000 Treasury bond paying 5% could be bought for $25,000 in the ensuing panic. Remember, you have to have access to cash money to buy.

The damage and destruction would be over in a matter of weeks. From there, the bond market could be back to normal. So if the interest rate dropped back down to 5% the bond you purchased for $25,000 would now be worth $100,000 ---- a chance to quadruple your savings.

Sound far fetched? History doesn't quite repeat itself. Are you ready for the ride? ---The ride that will be "different this time?"

Cash will be King. For how long is anyone's guess. Are you ready for it?

Monday, September 18, 2006

Real Estate, Its Getting Worse

My sister and her husband have been selling real estate in Colorado very successfully for the last 10 years. Now, this year, between the two of them, one sale so far this year, and that's it.

Colorado is not in the big player market, we are talking 150k to 200k per house. Foreclosures are at a record high level.

Now travel to California and look at houses in San Marcos for $800,000. You can rent them from $1800 to $2400 per month. If you bought a house at $800,000, and make $60,000 a year, then you're in a world of hurt. Your problems get worse when filing for bankruptcy and you have to show the documentation for your "No Doc Loan."

Well, all I can say, is that the warm and fuzzy feeling isn't so warm and fuzzy for a lot of people. The fuzzy part is getting fuzzier!

Colorado is not in the big player market, we are talking 150k to 200k per house. Foreclosures are at a record high level.

Now travel to California and look at houses in San Marcos for $800,000. You can rent them from $1800 to $2400 per month. If you bought a house at $800,000, and make $60,000 a year, then you're in a world of hurt. Your problems get worse when filing for bankruptcy and you have to show the documentation for your "No Doc Loan."

Well, all I can say, is that the warm and fuzzy feeling isn't so warm and fuzzy for a lot of people. The fuzzy part is getting fuzzier!

My Neighborhood is Weirding Out!

I was driving home from the supermarket Saturday afternoon. Couldn't believe all of the sign wavers. Here is three in a group on Mission and Las Posas. On the last mile to my house, I must have passed eight sign twirlers on various corners of Las Posas Avenue alone.

There are a lot of for sale signs in our area. This one seemed to go the extra mile. The newspapers stacked in the driveway didn't photograph very well. To be fair, there is a "Sale Pending" on the sign. I can't figure out why the recent addition of the garage banner and the "Reduced" sign if thats the case.

The neighbor a few doors down recently "harvested" his lawn. It could have been winter wheat. He probably cut the lawn so you could see the "For Rent" sign. At first it had $1895 per month, then a week later it went to $2295 per month. Last week it went for $790 for a room (master bedroom with own bath). The signs gone so I guess the owner has someone living in his master bedroom.

There are a lot of for sale signs in our area. This one seemed to go the extra mile. The newspapers stacked in the driveway didn't photograph very well. To be fair, there is a "Sale Pending" on the sign. I can't figure out why the recent addition of the garage banner and the "Reduced" sign if thats the case.

The neighbor a few doors down recently "harvested" his lawn. It could have been winter wheat. He probably cut the lawn so you could see the "For Rent" sign. At first it had $1895 per month, then a week later it went to $2295 per month. Last week it went for $790 for a room (master bedroom with own bath). The signs gone so I guess the owner has someone living in his master bedroom.

Tuesday, September 05, 2006

Things that go Bump in the Night

These are things that can keep you awake at night.

Ever heard of a big mutual fund going bankrupt? Even if you haven't, do you know the name of the one you own?

What happens when the baby boomers retire and ask for their money, is it there? It doesn't have to be there. They haven't asked for it (yet)! Your fund manager could be on his second tour around the world on his (yours technically) private yacht.

Ever heard of a retirement fund insured by the FDIC? Does it matter? They don't insure investment losses anyway.

After 34 pretty good years, isn't the stock market due for a 5 to 10 year downward slide?

Why would the big boys be buying 30 year bonds for less that the 5 year bonds--how much lower can interest rates go before you say, spend it, inflation will eat it up?

How can a hurricane triple insurance rates in Florida, but yet the threat of a housing collapse has inverted the interest yield curve?

An ad on the radio today advertises 5.9% fixed for 30 years 1.2 million limit, no income verification. Is this your retirement income in action?

How can Fannie Mae package a ton of junk and have no problem selling it? Nobody mentioned that "Risk had left the market."

There is a shoe ready to DROP, not sure what it will be, but it WILL go BUMP in the night.

Ever heard of a big mutual fund going bankrupt? Even if you haven't, do you know the name of the one you own?

What happens when the baby boomers retire and ask for their money, is it there? It doesn't have to be there. They haven't asked for it (yet)! Your fund manager could be on his second tour around the world on his (yours technically) private yacht.

Ever heard of a retirement fund insured by the FDIC? Does it matter? They don't insure investment losses anyway.

After 34 pretty good years, isn't the stock market due for a 5 to 10 year downward slide?

Why would the big boys be buying 30 year bonds for less that the 5 year bonds--how much lower can interest rates go before you say, spend it, inflation will eat it up?

How can a hurricane triple insurance rates in Florida, but yet the threat of a housing collapse has inverted the interest yield curve?

An ad on the radio today advertises 5.9% fixed for 30 years 1.2 million limit, no income verification. Is this your retirement income in action?

How can Fannie Mae package a ton of junk and have no problem selling it? Nobody mentioned that "Risk had left the market."

There is a shoe ready to DROP, not sure what it will be, but it WILL go BUMP in the night.

Monday, September 04, 2006

The Interest Rate Squeeze

There is a lot being said about the real estate bubble and whether or not it has popped. The issue here, is the sellers. They don't want to loose any money on a real estate sales transaction and\or want that dream price they saw last year ("In their hearts, they know they deserve it!")

So if they still have their job and have say 5 credit cards, there is no real problem with the mortgage. $50,000 in credit available ($10,000 per card) gives them one to two years to ride out the popping bubble. Then figure another 9 months for the bank to foreclose in the worst case scenario.

Up to now, people have been refinancing and paying off their credit cards with cheaper home equity line of credit money (HELOC). Here is where it gets interesting. The credit card companies advance more credit to more people. Then, there is a need for additional capital. This call for capital will result in lenders offering more interest for deposit money. Bank credit card loans are currently returning %18. Ever notice how those rates are listed as Prime plus some number? Raising the prime would be considered a "happy event" for the banks. I can see Bernanke biting into that credit bubble--go get 'em Ben, the banks will love you!

I'd like to see Master Card package a million in debt and turn it over to Fannie Mae for cash (the way the banks do with real estate)(my attempt at a very absurd train of thought).

The real estate cash infusion into our markets, spawned by Fannie Mae refunding, is drying up. The need for new additional capital to keep the ball rolling, will be have to be created in part, by increased interest rates. Where this new money is to come from, is the real question, we're all tapped out.

So if they still have their job and have say 5 credit cards, there is no real problem with the mortgage. $50,000 in credit available ($10,000 per card) gives them one to two years to ride out the popping bubble. Then figure another 9 months for the bank to foreclose in the worst case scenario.

Up to now, people have been refinancing and paying off their credit cards with cheaper home equity line of credit money (HELOC). Here is where it gets interesting. The credit card companies advance more credit to more people. Then, there is a need for additional capital. This call for capital will result in lenders offering more interest for deposit money. Bank credit card loans are currently returning %18. Ever notice how those rates are listed as Prime plus some number? Raising the prime would be considered a "happy event" for the banks. I can see Bernanke biting into that credit bubble--go get 'em Ben, the banks will love you!

I'd like to see Master Card package a million in debt and turn it over to Fannie Mae for cash (the way the banks do with real estate)(my attempt at a very absurd train of thought).

The real estate cash infusion into our markets, spawned by Fannie Mae refunding, is drying up. The need for new additional capital to keep the ball rolling, will be have to be created in part, by increased interest rates. Where this new money is to come from, is the real question, we're all tapped out.

Sunday, September 03, 2006

Famous Quotes from the Past

Here is something that I ran across that seems like a parallel to todays mindset.

This is a link to the site: http://www.gold-eagle.com/editorials_01/seymour062001.html

Begin Copied Material:

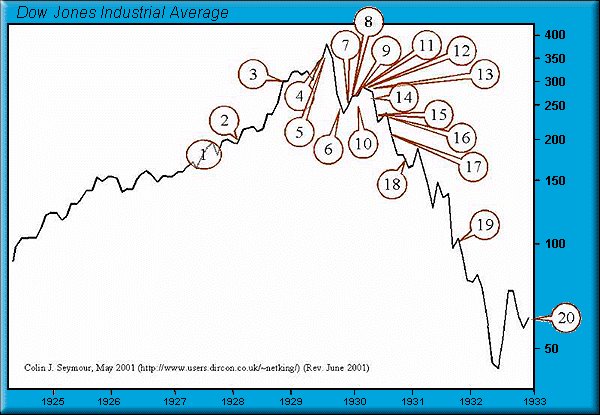

1927-1933 Chart of Pompous Prognosticators

1. "We will not have any more crashes in our time."

- John Maynard Keynes in 1927

2. "I cannot help but raise a dissenting voice to statements that we are living in a fool's paradise, and that prosperity in this country must necessarily diminish and recede in the near future."

- E. H. H. Simmons, President, New York Stock Exchange, January 12, 1928

"There will be no interruption of our permanent prosperity."

- Myron E. Forbes, President, Pierce Arrow Motor Car Co., January 12, 1928

3. "No Congress of the United States ever assembled, on surveying the state of the Union, has met with a more pleasing prospect than that which appears at the present time. In the domestic field there is tranquility and contentment...and the highest record of years of prosperity. In the foreign field there is peace, the goodwill which comes from mutual understanding."

- Calvin Coolidge December 4, 1928

4. "There may be a recession in stock prices, but not anything in the nature of a crash."

- Irving Fisher, leading U.S. economist , New York Times, Sept. 5, 1929

5. "Stock prices have reached what looks like a permanently high plateau. I do not feel there will be soon if ever a 50 or 60 point break from present levels, such as (bears) have predicted. I expect to see the stock market a good deal higher within a few months."

- Irving Fisher, Ph.D. in economics, Oct. 17, 1929

"This crash is not going to have much effect on business."

- Arthur Reynolds, Chairman of Continental Illinois Bank of Chicago, October 24, 1929

"There will be no repetition of the break of yesterday... I have no fear of another comparable decline."

- Arthur W. Loasby (President of the Equitable Trust Company), quoted in NYT, Friday, October 25, 1929

"We feel that fundamentally Wall Street is sound, and that for people who can afford to pay for them outright, good stocks are cheap at these prices."

- Goodbody and Company market-letter quoted in The New York Times, Friday, October 25, 1929

6. "This is the time to buy stocks. This is the time to recall the words of the late J. P. Morgan... that any man who is bearish on America will go broke. Within a few days there is likely to be a bear panic rather than a bull panic. Many of the low prices as a result of this hysterical selling are not likely to be reached again in many years."

- R. W. McNeel, market analyst, as quoted in the New York Herald Tribune, October 30, 1929

"Buying of sound, seasoned issues now will not be regretted"

- E. A. Pearce market letter quoted in the New York Herald Tribune, October 30, 1929

"Some pretty intelligent people are now buying stocks... Unless we are to have a panic -- which no one seriously believes, stocks have hit bottom."

- R. W. McNeal, financial analyst in October 1929

7. "The decline is in paper values, not in tangible goods and services...America is now in the eighth year of prosperity as commercially defined. The former great periods of prosperity in America averaged eleven years. On this basis we now have three more years to go before the tailspin."

- Stuart Chase (American economist and author), NY Herald Tribune, November 1, 1929

"Hysteria has now disappeared from Wall Street."

- The Times of London, November 2, 1929

"The Wall Street crash doesn't mean that there will be any general or serious business depression... For six years American business has been diverting a substantial part of its attention, its energies and its resources on the speculative game... Now that irrelevant, alien and hazardous adventure is over. Business has come home again, back to its job, providentially unscathed, sound in wind and limb, financially stronger than ever before."

- Business Week, November 2, 1929

"...despite its severity, we believe that the slump in stock prices will prove an intermediate movement and not the precursor of a business depression such as would entail prolonged further liquidation..."

- Harvard Economic Society (HES), November 2, 1929

8. "... a serious depression seems improbable; [we expect] recovery of business next spring, with further improvement in the fall."

- HES, November 10, 1929

"The end of the decline of the Stock Market will probably not be long, only a few more days at most."

- Irving Fisher, Professor of Economics at Yale University, November 14, 1929

"In most of the cities and towns of this country, this Wall Street panic will have no effect."

- Paul Block (President of the Block newspaper chain), editorial, November 15, 1929

"Financial storm definitely passed."

- Bernard Baruch, cablegram to Winston Churchill, November 15, 1929

9. "I see nothing in the present situation that is either menacing or warrants pessimism... I have every confidence that there will be a revival of activity in the spring, and that during this coming year the country will make steady progress."

- Andrew W. Mellon, U.S. Secretary of the Treasury December 31, 1929

"I am convinced that through these measures we have reestablished confidence."

- Herbert Hoover, December 1929

"[1930 will be] a splendid employment year."

- U.S. Dept. of Labor, New Year's Forecast, December 1929

10. "For the immediate future, at least, the outlook (stocks) is bright."

- Irving Fisher, Ph.D. in Economics, in early 1930

11. "...there are indications that the severest phase of the recession is over..."

- Harvard Economic Society (HES) Jan 18, 1930

12. "There is nothing in the situation to be disturbed about."

- Secretary of the Treasury Andrew Mellon, Feb 1930

13. "The spring of 1930 marks the end of a period of grave concern...American business is steadily coming back to a normal level of prosperity."

- Julius Barnes, head of Hoover's National Business Survey Conference, Mar 16, 1930

"... the outlook continues favorable..."

- HES Mar 29, 1930

14 "... the outlook is favorable..."

- HES Apr 19, 1930

15. "While the crash only took place six months ago, I am convinced we have now passed through the worst -- and with continued unity of effort we shall rapidly recover. There has been no significant bank or industrial failure. That danger, too, is safely behind us."

- Herbert Hoover, President of the United States, May 1, 1930

"...by May or June the spring recovery forecast in our letters of last December and November should clearly be apparent..."

- HES May 17, 1930

"Gentleman, you have come sixty days too late. The depression is over."

- Herbert Hoover, responding to a delegation requesting a public works program to help speed the recovery, June 1930

16. "... irregular and conflicting movements of business should soon give way to a sustained recovery..."

- HES June 28, 1930

17. "... the present depression has about spent its force..."

- HES, Aug 30, 1930

18. "We are now near the end of the declining phase of the depression."

- HES Nov 15, 1930

19. "Stabilization at [present] levels is clearly possible."

- HES Oct 31, 1931

20. "All safe deposit boxes in banks or financial institutions have been sealed... and may only be opened in the presence of an agent of the I.R.S."

- President F.D. Roosevelt, 1933

End Copied Material

Quotes #5 and #8 are very famous remarks by Irving Fisher, who at the time was managing the Yale endowment funds. It didn't go well from there.

These were very intelligent people back in their time. Their thoughts on what would happen next were way off the mark. What was said, sounded good and was reassuring.

It leaves a lot of doubt about what you can take for granted in todays newspapers

Note, quote 20 refers to the fact that it became illegal to own gold as an American citizen. The government was making sure no one was holding out on them. You had to trade your gold in for currency. This was FDR's way of keeping everyone honest--government excluded.

This is a link to the site: http://www.gold-eagle.com/editorials_01/seymour062001.html

Begin Copied Material:

1927-1933 Chart of Pompous Prognosticators

1. "We will not have any more crashes in our time."

- John Maynard Keynes in 1927

2. "I cannot help but raise a dissenting voice to statements that we are living in a fool's paradise, and that prosperity in this country must necessarily diminish and recede in the near future."

- E. H. H. Simmons, President, New York Stock Exchange, January 12, 1928

"There will be no interruption of our permanent prosperity."

- Myron E. Forbes, President, Pierce Arrow Motor Car Co., January 12, 1928

3. "No Congress of the United States ever assembled, on surveying the state of the Union, has met with a more pleasing prospect than that which appears at the present time. In the domestic field there is tranquility and contentment...and the highest record of years of prosperity. In the foreign field there is peace, the goodwill which comes from mutual understanding."

- Calvin Coolidge December 4, 1928

4. "There may be a recession in stock prices, but not anything in the nature of a crash."

- Irving Fisher, leading U.S. economist , New York Times, Sept. 5, 1929

5. "Stock prices have reached what looks like a permanently high plateau. I do not feel there will be soon if ever a 50 or 60 point break from present levels, such as (bears) have predicted. I expect to see the stock market a good deal higher within a few months."

- Irving Fisher, Ph.D. in economics, Oct. 17, 1929

"This crash is not going to have much effect on business."

- Arthur Reynolds, Chairman of Continental Illinois Bank of Chicago, October 24, 1929

"There will be no repetition of the break of yesterday... I have no fear of another comparable decline."

- Arthur W. Loasby (President of the Equitable Trust Company), quoted in NYT, Friday, October 25, 1929

"We feel that fundamentally Wall Street is sound, and that for people who can afford to pay for them outright, good stocks are cheap at these prices."

- Goodbody and Company market-letter quoted in The New York Times, Friday, October 25, 1929

6. "This is the time to buy stocks. This is the time to recall the words of the late J. P. Morgan... that any man who is bearish on America will go broke. Within a few days there is likely to be a bear panic rather than a bull panic. Many of the low prices as a result of this hysterical selling are not likely to be reached again in many years."

- R. W. McNeel, market analyst, as quoted in the New York Herald Tribune, October 30, 1929

"Buying of sound, seasoned issues now will not be regretted"

- E. A. Pearce market letter quoted in the New York Herald Tribune, October 30, 1929

"Some pretty intelligent people are now buying stocks... Unless we are to have a panic -- which no one seriously believes, stocks have hit bottom."

- R. W. McNeal, financial analyst in October 1929

7. "The decline is in paper values, not in tangible goods and services...America is now in the eighth year of prosperity as commercially defined. The former great periods of prosperity in America averaged eleven years. On this basis we now have three more years to go before the tailspin."

- Stuart Chase (American economist and author), NY Herald Tribune, November 1, 1929

"Hysteria has now disappeared from Wall Street."

- The Times of London, November 2, 1929

"The Wall Street crash doesn't mean that there will be any general or serious business depression... For six years American business has been diverting a substantial part of its attention, its energies and its resources on the speculative game... Now that irrelevant, alien and hazardous adventure is over. Business has come home again, back to its job, providentially unscathed, sound in wind and limb, financially stronger than ever before."

- Business Week, November 2, 1929

"...despite its severity, we believe that the slump in stock prices will prove an intermediate movement and not the precursor of a business depression such as would entail prolonged further liquidation..."

- Harvard Economic Society (HES), November 2, 1929

8. "... a serious depression seems improbable; [we expect] recovery of business next spring, with further improvement in the fall."

- HES, November 10, 1929

"The end of the decline of the Stock Market will probably not be long, only a few more days at most."

- Irving Fisher, Professor of Economics at Yale University, November 14, 1929

"In most of the cities and towns of this country, this Wall Street panic will have no effect."

- Paul Block (President of the Block newspaper chain), editorial, November 15, 1929

"Financial storm definitely passed."

- Bernard Baruch, cablegram to Winston Churchill, November 15, 1929

9. "I see nothing in the present situation that is either menacing or warrants pessimism... I have every confidence that there will be a revival of activity in the spring, and that during this coming year the country will make steady progress."

- Andrew W. Mellon, U.S. Secretary of the Treasury December 31, 1929

"I am convinced that through these measures we have reestablished confidence."

- Herbert Hoover, December 1929

"[1930 will be] a splendid employment year."

- U.S. Dept. of Labor, New Year's Forecast, December 1929

10. "For the immediate future, at least, the outlook (stocks) is bright."

- Irving Fisher, Ph.D. in Economics, in early 1930

11. "...there are indications that the severest phase of the recession is over..."

- Harvard Economic Society (HES) Jan 18, 1930

12. "There is nothing in the situation to be disturbed about."

- Secretary of the Treasury Andrew Mellon, Feb 1930

13. "The spring of 1930 marks the end of a period of grave concern...American business is steadily coming back to a normal level of prosperity."

- Julius Barnes, head of Hoover's National Business Survey Conference, Mar 16, 1930

"... the outlook continues favorable..."

- HES Mar 29, 1930

14 "... the outlook is favorable..."

- HES Apr 19, 1930

15. "While the crash only took place six months ago, I am convinced we have now passed through the worst -- and with continued unity of effort we shall rapidly recover. There has been no significant bank or industrial failure. That danger, too, is safely behind us."

- Herbert Hoover, President of the United States, May 1, 1930

"...by May or June the spring recovery forecast in our letters of last December and November should clearly be apparent..."

- HES May 17, 1930

"Gentleman, you have come sixty days too late. The depression is over."

- Herbert Hoover, responding to a delegation requesting a public works program to help speed the recovery, June 1930

16. "... irregular and conflicting movements of business should soon give way to a sustained recovery..."

- HES June 28, 1930

17. "... the present depression has about spent its force..."

- HES, Aug 30, 1930

18. "We are now near the end of the declining phase of the depression."

- HES Nov 15, 1930

19. "Stabilization at [present] levels is clearly possible."

- HES Oct 31, 1931

20. "All safe deposit boxes in banks or financial institutions have been sealed... and may only be opened in the presence of an agent of the I.R.S."

- President F.D. Roosevelt, 1933

End Copied Material

Quotes #5 and #8 are very famous remarks by Irving Fisher, who at the time was managing the Yale endowment funds. It didn't go well from there.

These were very intelligent people back in their time. Their thoughts on what would happen next were way off the mark. What was said, sounded good and was reassuring.

It leaves a lot of doubt about what you can take for granted in todays newspapers

Note, quote 20 refers to the fact that it became illegal to own gold as an American citizen. The government was making sure no one was holding out on them. You had to trade your gold in for currency. This was FDR's way of keeping everyone honest--government excluded.

Subscribe to:

Posts (Atom)